Yeni başlayanlar için kılavuz

Ders 2

Fundamentals of Quantitative Models and Intelligent Investment Systems

As AI begins to enter the financial markets, a core question arises: How exactly does AI participate in investing? The answer is not simply relying on a chatbot or prediction model, but rather a comprehensive intelligent investment system composed of data, algorithms, strategies, and risk control. At the heart of this foundation is quantitative investing.

What Is Quantitative Investing and Its Core Framework

Quantitative investing is essentially a method of analyzing and trading markets using mathematical models, statistical methods, and programmed systems. Unlike traditional investing, which relies on subjective judgment, quantitative investing emphasizes rules-based and data-driven approaches, requiring all trading logic to be converted into conditions executable by programs.

A complete quantitative system typically consists of the following components:

-

Data acquisition

-

Signal generation

-

Strategy execution

-

Risk control

-

Performance evaluation

These modules together form a closed-loop automated investment system.

For example, when the system detects that a certain asset simultaneously meets the following conditions:

-

Decreasing volatility

-

Increasing capital inflows

-

Strengthening market sentiment

The model may automatically generate a buy signal without requiring manual analysis.

As market complexity increases, modern quantitative systems have evolved beyond simple program trading and now function more like continuously learning financial decision-making systems.

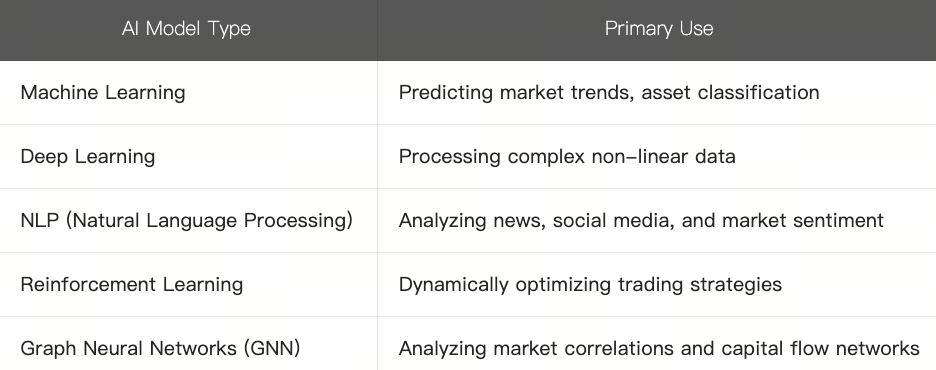

Common Applications of AI Models in Finance

AI applications in financial markets are not based on a single technology, but are the result of multiple models working together. Different models are suited to different problems. For instance, some models excel at predicting price trends, while others are better at analyzing news sentiment or identifying abnormal risks.

Currently, commonly used AI technologies in finance can be roughly categorized as follows:

Natural Language Processing and AI in Financial Markets

Among these, the development of natural language processing has had a particularly significant impact on financial markets. In the past, researchers had to manually read large volumes of news and financial reports; now, AI can automatically analyze:

-

Changes in news tone

-

Sentiment on social media

-

Key points in company announcements

-

Directions of macroeconomic policy

This has further accelerated the speed at which the market responds to information.

At the same time, reinforcement learning models are also being applied to dynamic trading systems. Unlike traditional fixed rules, these models continuously adjust their strategies based on market feedback, similar to traders in ongoing training.

Factor Models and Machine Learning Strategies

In quantitative investment systems, factors have always been a core concept. A factor can be understood as a quantifiable characteristic that affects asset price movements. In the past, quantitative investment mostly revolved around building trading logic and asset allocation strategies based on specific factors.

Common traditional factors include momentum, value, volatility, and market capitalization factors. For example, the momentum factor assumes that upward trends may continue; the value factor tends to look for undervalued assets; while volatility and market capitalization factors focus on the impact of market risk and asset size on returns, respectively.

Previously, these factor models were mainly constructed using financial theory, statistical methods, and the experience of investment managers. In other words, researchers would first propose a hypothesis and then verify its validity through historical data. However, with the introduction of AI and machine learning technologies into quantitative investing, this logic has begun to change. Today's models no longer just use existing factors—they can proactively discover factors from massive datasets.

For example, a machine learning model might identify hidden correlations between certain market sentiments and price fluctuations or recognize relationships between specific capital flows and the probability of asset appreciation. The model can even dynamically assess which factors remain effective and which have become obsolete under different macroeconomic conditions.

This means AI's role is no longer limited to executing existing strategies but is continuously uncovering new market patterns and constantly adjusting its own decision logic. However, this capability also introduces new challenges. Because machine learning models are highly skilled at finding patterns in data, they may sometimes identify seemingly effective rules that are actually historical coincidences. In other words, the model might simply memorize historical data rather than truly understand market logic.

Modern AI quantitative systems increasingly emphasize factor stability, model generalization ability, and adaptability to different market environments. Only models that can remain effective across cycles and markets have the potential to operate in real markets over the long term.

Risk Control and Backtesting Mechanisms

There is a classic saying in quantitative investing: any strategy can make money—until it actually enters the market. What this reflects is the critical importance of risk control.

An outstanding intelligent investment system is not just about trading—it is even more about managing risk. Long-term performance is often determined not by single returns but by whether the system can survive extreme market conditions. Therefore, risk control typically runs through the entire AI investment system. The most fundamental aspect is position management: the system must decide how much capital to allocate to each trade to avoid excessive concentration of risk due to fluctuations in a single asset. Additionally, when abnormal market volatility occurs, the system automatically reduces risk exposure through stop-loss and risk control rules—for example, by reducing positions, pausing trading, or increasing cash holdings to prevent further losses from dramatic market changes.

Correlation control is also a crucial part of quantitative investing. Many assets may appear diversified on the surface but can move in high correlation under market stress. If the system cannot identify true relationships between assets, there is a risk of apparent diversification but actual concentration.

Besides real-time risk management, backtesting is also an indispensable mechanism in quantitative systems. Backtesting involves using historical market data to simulate past performance of a strategy to verify its effectiveness.

A complete backtesting process usually includes importing historical data, establishing strategy rules, simulating historical trading processes, calculating return and risk indicators, and analyzing strategy stability. Through these processes, developers can better understand how models perform during different market phases.

However, backtesting has its limitations. Historical performance does not guarantee future results. Many models perform exceptionally well on historical data but fail quickly when deployed in real markets—a situation commonly referred to as overfitting. To mitigate this risk, modern AI investment systems increasingly stress multi-market testing, validation across different cycles, stress testing, and simulations of extreme market scenarios. Only models that can adapt to complex market environments and maintain stability under various conditions have a better chance of operating over the long term.

Sorumluluk Reddi

Yasal Uyarı 1: Bu içerik yatırım tavsiyesi niteliği taşımamaktadır. Dijital varlıkların alım veya satımını teşvik etmeyi amaçlamaz ve yalnızca bilgilendirme amaçlıdır. Kripto varlıklar yüksek risk içerir ve önemli fiyat dalgalanmalarına maruz kalabilir. Herhangi bir yatırım kararı vermeden önce kendi mali durumunuzu değerlendirmeli ve kararınızı bağımsız olarak vermelisiniz.

Yasal Uyarı 2: Bu makalede yer alan veriler ve grafikler yalnızca genel bilgilendirme amaçlıdır. Tüm içerik özenle hazırlanmış olmakla birlikte, olası hata veya eksikliklerden dolayı sorumluluk kabul edilmemektedir. Gate TR Akademi ekibi bu içeriği farklı dillere çevirebilir. Çevrilen hiçbir makale izin alınmadan kopyalanamaz, çoğaltılamaz veya dağıtılamaz.

Dersler

Ders 1:The New Era of AI and Asset Allocation

1 Kursu bitiren

Ders 2:Fundamentals of Quantitative Models and Intelligent Investment Systems

0 Kursu bitiren

Ders 3:Gate AI and Smart Trading Ecosystem in Practice

0 Kursu bitiren

Ders 4:AI Investment Practices and On-Chain Data Applications

0 Kursu bitiren

Ders 5:Autonomous Investment Decision Systems and Future Financial Trends

1 Kursu bitiren

Diğer Kurslar

Beginner

The Beginner's Guide to Blockchain-based Airdrops

With the rapid development of the blockchain industry, an increasing number of projects choose to hold airdrops to expand their user base and reward early adopters. As a commonly-used marketing strategy, airdrops have not only provided users with opportunities to acquire cryptocurrencies but also offer project teams extensive exposure and the opportunity to expand their communities. Through this course, you will grasp the basic concepts of airdrops, understand different types of airdrop events, and master the skills and strategies for airdrop farming. This way, you will establish a solid foundation for your successful participation in blockchain-based airdrops.

Intermediate

Crypto Mining Equipment

This course covers everything you need to know about mining, from why mining is essential and what is the most helpful mining equipment for the future of crypto mining. We will go into various types of mining analyzing all the equipment like GPUs, CPUs, FPGAs, ASICs

Intermediate

Identity in Crypto: Main Projects

Welcome to the comprehensive course on "Identity in Crypto: Main Projects." In this cutting-edge course, we will embark on a journey to explore the fascinating realm of Identity Tokens within the cryptocurrency ecosystem. As the world embraces blockchain technology and decentralized applications, the importance of secure and verifiable identity solutions becomes paramount. This course will give you in-depth knowledge of Identity Tokens, their significance in the Web3 ecosystem, and their potential to revolutionize identity verification, privacy, and trust. Join us on this enlightening exploration, and equip yourself with the expertise to navigate the dynamic landscape of decentralized identity in the digital age.

Intermediate

Introduction to Masternode Tokens

Welcome to the "Introduction to Masternode Tokens" course! This comprehensive course is designed to provide you with a deep understanding of masternode tokens and their significance in the cryptocurrency ecosystem. Whether you are a beginner or an experienced crypto enthusiast, this course will equip you with the knowledge and skills to navigate the world of masternodes, explore popular masternode-based cryptocurrencies, and explore the fundamental concepts behind masternode networks. Join us on this exciting journey as we delve into the inner workings of masternode tokens and unlock the potential they hold in shaping the future of decentralized finance.

Beginner

Crypto Mining

In this course, you will learn everything you need to know about mining cryptocurrencies, including the different types of mining hardware, software tools, and strategies for reducing the environmental impact of mining. Whether you're a beginner or an experienced miner, this course will provide you with the knowledge and skills to succeed in this exciting and rapidly evolving industry.

Beginner

Learn about web3 data and analytics

In the Web3 Data course, we'll talk about the importance of on-chain data, its uses, and even prospective career paths. You'll also learn about how these analytical tools are created.