Yeni başlayanlar için kılavuz

What is the Regulatory Framework for Tokenized Stocks? Securities Law, Custody, and Compliance Structure Analysis.

Son Güncelleme 2026-06-24 06:20:35

Tokenized Stocks, one of the most closely watched applications in the Real World Assets (RWA) space, use blockchain technology to allow traditional stock assets to circulate on-chain as digital tokens. This enhances accessibility, composability, and global transfer efficiency.

However, stocks are inherently heavily regulated securities. When mapped onto a blockchain, their legal nature does not disappear simply because the technology changes. Therefore, securities laws, custody systems, and investor protection mechanisms form the foundation for tokenized stock development and determine whether a project can operate compliantly over the long term.

What Determines the Regulatory Attributes of Tokenized Stocks?

Regulators generally do not judge an asset's nature solely by its technical form. Instead, they focus on the economic rights the asset represents.

If token holders can obtain stock-related income rights, dividend rights, price exposure, or other securities attributes, regulators typically treat the token as a security. In other words, even if the asset runs on a blockchain, as long as it corresponds to stock rights, it may fall under the securities regulatory framework.

This approach means blockchain technology changes how assets are recorded and transferred, not their legal nature. Consequently, tokenized stocks often must meet compliance requirements similar to those for traditional securities.

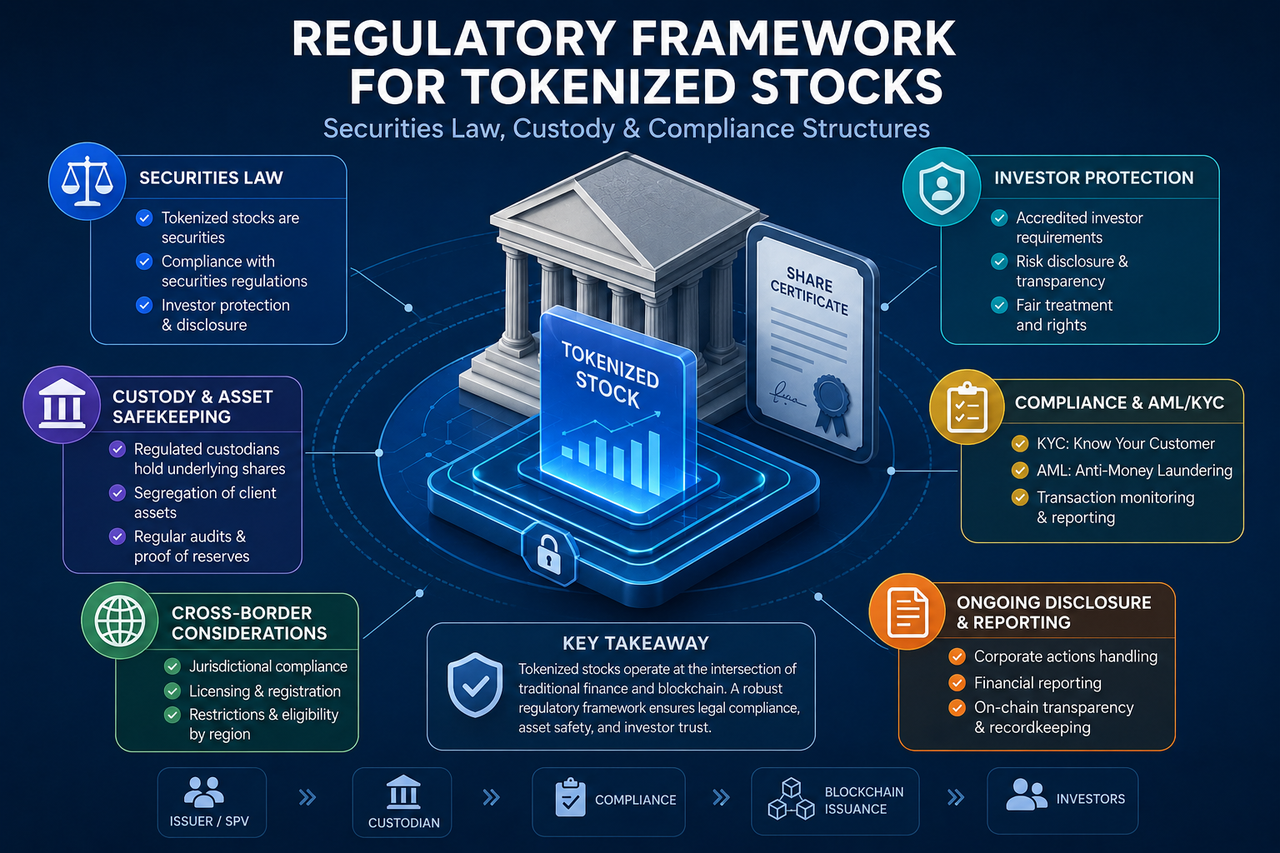

Why Is Securities Law the Core Regulatory Basis for Tokenized Stocks?

Securities law is the most critical legal foundation for tokenized stocks because they essentially involve the digital expression of stock-related rights.

In traditional financial markets, stock issuance must comply with disclosure requirements, investor suitability rules, and market oversight. When stocks are tokenized, these requirements generally extend to the on-chain environment rather than disappear.

Regulators focus on whether the issuer is legitimate, whether the underlying assets actually exist, whether investor rights are protected, and whether market manipulation risks exist. Therefore, most compliant tokenized stock projects design their legal frameworks around securities regulations.

What Legal Structures Are Commonly Used for Tokenized Stocks?

The legal structure defines the relationship between the token and the underlying asset and is a key focus of regulatory review.

Direct Shareholding Structure

In this model, the issuer holds the actual stocks and issues tokens in a set ratio. Theoretically, there is a clear mapping between the token and the underlying stock.

This structure offers high transparency but often involves complex legal requirements for cross-border issuance and shareholder registration.

Special Purpose Vehicle (SPV) Structure

SPV is one of the most common legal structures in tokenized stocks. The issuer typically holds stock assets through a separate legal entity, which then issues the corresponding tokens.

SPVs enable asset segregation and improve legal clarity, making them widely used for tokenizing private equity and shares of unlisted companies.

Derivatives Structure

Some tokenized stocks do not hold actual stocks. Instead, they track stock price performance through contracts or indices.

This model provides price exposure rather than actual shareholder rights. Therefore, it may be subject to both securities and derivatives regulations.

Why Is Asset Custody So Important?

Custody mechanisms determine whether the underlying assets truly exist and whether investor rights are protected.

In traditional securities markets, stocks are held by regulated custodians. Tokenized stocks face the same issue because an on-chain token is not the same as the actual stock.

If the issuer cannot prove the underlying assets are properly custodied, the mapping between token and stock becomes unverifiable. That is why compliant projects typically engage third-party custodians, auditors, and periodic disclosure mechanisms to enhance transparency and credibility.

What Role Do AML and KYC Play in Tokenized Stocks?

Anti-Money Laundering (AML) and Know Your Customer (KYC) are critical compliance components for tokenized stocks.

Traditional securities markets require investor identification and monitoring of abnormal trading. Tokenized stocks face similar requirements. Regulators want to prevent securities markets from being used for money laundering, fraud, or illegal fund transfers, so most compliant platforms require user identity verification.

In some jurisdictions, investor suitability checks are also mandatory. Some products are limited to accredited investors, while others may have investment thresholds based on local regulations.

What Regulatory Challenges Does Cross-Border Issuance Face?

Tokenized stocks are inherently global, but securities regulation is typically national or regional.

A single tokenized stock product may target investors from multiple countries, but jurisdictions differ on issuance rules, investor qualifications, and disclosure requirements. This inconsistency makes cross-border operations one of the most complex challenges in the space.

To reduce regulatory risk, many projects restrict participation from users in certain regions or use different legal structures and issuance methods for different markets.

How Do Tokenized Stocks and Traditional Stocks Differ in Regulation?

Both are subject to securities regulation, but they differ significantly in how assets move.

| Dimension | Traditional Stocks | Tokenized Stocks |

|---|---|---|

| Asset Recording | Central securities depository | Blockchain ledger |

| Trading Hours | Exchange business hours | Depends on structure |

| Custody Method | Brokerage and custodians | Custodian + on-chain assets |

| Compliance Requirements | Securities law | Securities law + digital asset regulation |

| Cross-Border Circulation | Relatively restricted | Theoretically more efficient |

Despite different technical forms, investor protection, disclosure, and market integrity remain common goals. Tokenized stocks are more an upgrade to securities market infrastructure than a replacement for the regulatory system.

Summary

Tokenized stocks combine traditional securities with blockchain technology, so their regulatory framework spans securities law, asset custody, AML, KYC, and investor protection. Whether on-chain or off, if an asset represents stock rights or stock value exposure, it generally must follow securities regulations.

From direct shareholding to SPVs to derivatives, different tokenized stock products use different legal designs. But underlying asset authenticity, custody transparency, and investor protection remain the core regulatory focus.

FAQs

Are tokenized stocks considered securities?

In most jurisdictions, if a tokenized stock represents stock rights or stock value exposure, regulators treat it as a security. Therefore, such projects typically must comply with securities laws.

Why is SPV often used for tokenized stocks?

An SPV (Special Purpose Vehicle) isolates the underlying assets from the issuer and creates a clear legal relationship. This makes it a common legal structure for tokenized stocks and RWA projects.

Do tokenized stocks require asset custody?

Yes. Custody proves the underlying stocks actually exist and is essential for investor protection. Without custody, the link between the token and the real asset weakens.

Why are KYC and AML applicable to tokenized stocks?

Tokenized stocks are regulated financial products, so KYC and AML procedures are usually required. These measures help verify investor identities and reduce the risk of money laundering and financial crime.

Can tokenized stocks completely replace traditional stocks?

Tokenized stocks change how assets are recorded and transferred, but they do not alter the legal nature of stocks. The regulatory, custody, and investor protection mechanisms of traditional securities markets remain essential for tokenized stocks to operate.

Yazar: Jayne

Sorumluluk Reddi

* Yasal Uyarı 1: Bu içerik, yatırım tavsiyesi niteliğinde değildir. Dijital varlık alım-satımını teşvik etmeyi amaçlamaz, yalnızca bilgilendirme amaçlıdır. Kripto varlıklar yüksek risk içerir ve ciddi fiyat dalgalanmalarına maruz kalabilir. Yatırım kararı vermeden önce kendi finansal durumunuzu değerlendirmeli ve kararınızı bağımsız olarak vermelisiniz.

* Yasal Uyarı 2: Makalede yer alan veriler ve grafikler yalnızca genel bilgilendirme amacıyla sunulmuştur. Tüm içerikler özenle hazırlanmış olsa da, olası hata veya eksikliklerden dolayı sorumluluk kabul edilmez. Gate TR Akademi ekibi bu içeriği farklı dillere çevirebilir. Hiçbir çeviri makale, kopyalanamaz, çoğaltılamaz veya izinsiz dağıtılamaz.

Paylaş

İçindekiler

What Determines the Regulatory Attributes of Tokenized Stocks?

Why Is Securities Law the Core Regulatory Basis for Tokenized Stocks?

What Legal Structures Are Commonly Used for Tokenized Stocks?

Why Is Asset Custody So Important?

What Role Do AML and KYC Play in Tokenized Stocks?

What Regulatory Challenges Does Cross-Border Issuance Face?

How Do Tokenized Stocks and Traditional Stocks Differ in Regulation?

Summary

FAQs

Sign Up

İlgili Makaleler

Beginner

How Does PAXG Work? In-Depth Overview of the Physical Gold Tokenization Mechanism

PAXG (Pax Gold) is a tokenized asset backed by physical gold, issued by the fintech company Paxos and traded on the Ethereum blockchain as an ERC-20 token. The core concept is to tokenize physical gold on-chain, with each PAXG token representing ownership of a certain amount of gold. This structure enables investors to hold and trade gold in the form of a digital asset.

2026-03-24 19:12:51

Beginner

How is the price of PAXG determined? Pegging mechanism, trading depth, and influencing factors

PAXG (Pax Gold) is a tokenized asset backed by physical gold reserves, launched by fintech firm Paxos and issued as an ERC-20 token on the Ethereum blockchain. The core concept is to digitally represent real-world gold assets, allowing investors to hold and trade gold via the blockchain network. Because each PAXG token corresponds to a specific quantity of physical gold, its price is theoretically expected to closely track the global gold market.

2026-03-24 19:11:40

Advanced

Gate Research: 2024 Cryptocurrency Market Review and 2025 Trend Forecast

This report provides a comprehensive analysis of the past year's market performance and future development trends from four key perspectives: market overview, popular ecosystems, trending sectors, and future trend predictions. In 2024, the total cryptocurrency market capitalization reached an all-time high, with Bitcoin surpassing $100,000 for the first time. On-chain Real World Assets (RWA) and the artificial intelligence sector experienced rapid growth, becoming major drivers of market expansion. Additionally, the global regulatory landscape has gradually become clearer, laying a solid foundation for market development in 2025.

2026-03-24 11:56:16

Intermediate

What Are the Risks of TSLA? Understanding Tesla’s Competitive Landscape and Investment Challenges

The main investment risks of TSLA come from intensifying industry competition, pricing pressure, swings in profitability, and changes in market valuation. As one of the global leaders in the new energy vehicle industry, Tesla has strong brand and technology advantages, but it still faces mounting competition from both traditional automakers and emerging EV brands. When evaluating TSLA, investors should pay close attention to Tesla’s market share, margin trends, technological progress, and the broader market environment in order to form a more complete view of its long-term investment value and risk.

2026-04-21 06:59:56

Beginner

GoldFinger Use Cases in DeFi: How Gold Assets Enter the On-chain Financial System

Through asset tokenization and a Proof of Reserve mechanism, GoldFinger brings gold into the DeFi ecosystem, allowing it to take part in on-chain financial activity as collateral, a liquidity tool, and a component of yield strategies. Once tokenized, gold assets such as ART can function as collateral, liquidity instruments, and building blocks in yield strategies across lending markets, decentralized exchanges, and structured returns, turning a traditional store of value into composable on-chain financial infrastructure.

2026-04-15 03:47:31

Beginner

How Does GoldFinger Work? Gold Asset Tokenization, Proof of Reserve, and on-chain Circulation Explained

GoldFinger operates through a process that includes asset custody, Proof of Reserve, token minting, and on-chain circulation. By placing physical gold within a compliant custody framework and mapping it on-chain through ART tokens, GoldFinger turns gold into a digital, programmable asset. At the same time, its Proof of Reserve mechanism ensures that on-chain tokens correspond to the underlying assets, supporting trading, collateralization, and redemption in DeFi scenarios.

2026-04-15 03:01:54